A big part of the American dream is owning your own home. It is something that everybody strives for and hopes to one day accomplish. However, most people cannot afford to pay cash for a home, instead requiring the use of a mortgage from a bank. Of course, a mortgage comes with high monthly payments that can sometimes be difficult to make. If you continuously miss payments, you will find yourself in foreclosure. Knowing the most common causes of foreclosure can help you to prevent it from happening to you.

What Is Foreclosure?

First, let’s make sure that you have a full understanding of what foreclosure is. Foreclosure is the legal process in which your lender seizes a property (usually your home) because you have defaulted on your mortgage payments. The lender then sells the home to recover the outstanding loan balance, and you are forced to vacate. Basically, foreclosure means that you have not paid your mortgage and the bank is taking your home. This usually happens after 3-4 months of missed mortgage payments. Prior to foreclosure, the lender will always send notices warning of default and giving you time to catch up on payments or seek loan relief.

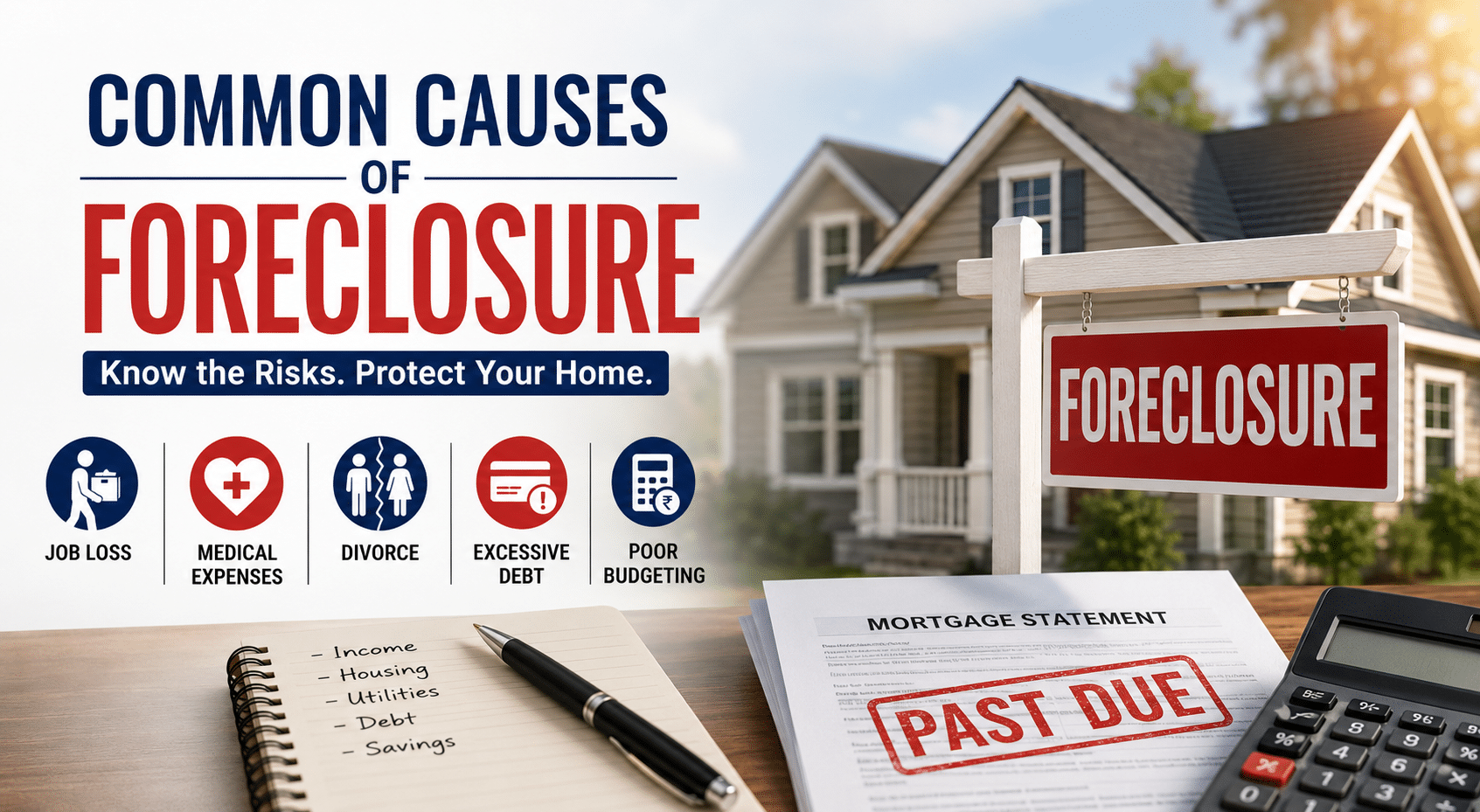

Cause #1: Job Loss

This may be the most common cause of foreclosure. There have already been 5.2 million layoffs in 2026. When a person is laid off or fired, their income ceases. They may be able to receive unemployment payments, but these are temporary and are usually not anywhere close to the amount they were paid at their job. Without steady income, it can become impossible to make your mortgage payment, which is usually the largest bill you will have. Even if you have savings, it is quite easy to burn through them before you find a new job.

Cause #2: Medical Expenses and Health Emergencies

If there is one thing you can’t predict it is medical expenses. Surgery, emergency room visits, and medications can create a massive financial burden. Trying to pay off medical bills while also paying a mortgage can be extremely difficult. Not to mention, this difficulty is compounded if the medical emergency in question prevents you from working. It is quite common for a person to have a medical emergency and end up in foreclosure within a matter of months.

Cause #3: Divorce

Oftentimes in divorce, one spouse keeps the house. While this can seem like a win, it can also create serious financial hardship. The house was likely purchased under the assumption that two incomes would be available to help pay for it. Now, with only a single income, mortgage payments can become difficult, if not impossible, to make. There are also legal costs and possible child support to consider, which can further place strain on your financial situation. Sadly, foreclosure following a divorce is extremely common.

Cause #4: Excessive Consumer Debt

With all of the things available for purchase today, it is very easy to rack up large debt on credit cards. When this happens, it creates feelings of stress and anxiety, which causes people to want to prioritize paying down their credit card debt. While getting rid of credit card debt is a smart financial move, it should not be done at the expense of your mortgage payments. It is all too common that a person misses mortgage payments because they wanted to clear their credit card debt.

Cause #5: Poor Budgeting

No amount of income can make up for poor budgeting skills. It is actually quite common for a household to not even have a budget. This is a huge risk. If you are not paying attention to how much you are spending, it is very easy to burn through your income. This can lead to you simply not having the money to make your mortgage payment when it is due. Have this happen multiple months in a row and you will be in foreclosure before you know it. Luckily, the Federal Trade Commission has a budget worksheet you can use to make a household budget and prevent this from happening.

Warning Signs That Foreclosure Risk May Be Increasing

It is important that you know when foreclosure is coming. This will allow you to take action before it is too late. Signs that the risk of foreclosure is increasing include:

- Missed Mortgage Payments: This may seem obvious, but it is important to mention. Remember, one missed payment is manageable. More than that and you are at serious risk of foreclosure.

- Falling Behind on Other Bills: Your mortgage is just one bill. You also have auto loans, utilities, credit card bills, and more. If you start falling behind on these other bills, it means that your financial situation has become precarious. You need to start budgeting or soon it will be your mortgage payments you are missing, which will lead to foreclosure.

- Foreclosure Notices: Your lender will let you know that foreclosure is coming. You will get delinquency notices in the mail. These will warn you that you have missed payments and that foreclosure is imminent. Many homeowners make the mistake of thinking these are empty threats. They most definitely are not. If you are receiving these notices, you need to take action to do something about your situation. Failure to do so will absolutely lead to foreclosure.

Keep an eye out for these warning signs. Recognizing them will allow you to take certain actions that can prevent foreclosure or even stop a foreclosure that has begun.

Preventing Foreclosure

If you’ve started receiving foreclosure warnings, you are not out of options. First, you should contact your lender. They may be open to loan modification, where they change the terms of your loan to make your payments more affordable. If this fails, your best option may be Chapter 13 bankruptcy, which allows individuals with regular income to restructure their debts through a court-approved installment plan lasting three to five years. When you declare Chapter 13 bankruptcy, all collection efforts are paused, including foreclosure. If you go this route, be sure to hire a Chapter 13 bankruptcy attorney. They will be able to get the process started quickly, ensuring you are able to save your home.