If you want to invest a lump sum and expecting to get good regular income from mutual funds, you can opt for Monthly Income Plan (MIP) Mutual funds in India. MIP Mutual Funds objective is to invest some portion in equity markets and majority in debt related instruments. MIP Mutual funds provide higher returns compared to Bank Fixed Deposits and post office MIS schemes. Some of the top MIP Funds have provided 14% annualized returns too. What are Monthly Income Plan (MIP) Mutual Funds in India? How are they different from Bank Monthly Income Plan Schemes or Post Office MIS Scheme? Which are the top 10 Monthly Income Plan (MIP) Mutual funds to invest in 2017 in India?

Also Read: Best Sector Based Mutual Funds to invest now

What are Monthly Income Plan (MIP) Mutual Funds?

Monthly Income Plans (MIP) mutual funds are debt funds which invests 5% to 30% in equity and balance in debt related instruments. These MIP Mutual Funds provide regular dividend payouts either by monthly, quarterly or half yearly.

What are key features of MIP mutual funds?

Here are some of the key features of MIP Mutual Funds.

1) If you want to invest lump sum investment and expecting regular returns, MIP mutual funds are one of the best options.

2) They would provide regular payouts in the form of dividend. Though not guaranteed, they offer the highest returns compared to bank FD’s.

3) MIP returns are volatile as it invests part of the amount in equity.

4) Under MIP, Post tax returns are high as these are classified under debt schemes and returns are taxed with or without indexation method.

5) Like any other mutual fund, MIP’s are available in growth and dividend option. However, growth option does not make any sense as the purpose is for regular payouts.

How does Dividend and Growth Option work in MIP Mutual Funds?

If you invest in MIP mutual funds through dividend option, you would get a regular dividend either by monthly, quarterly or half yearly. These dividends are paid only from your capital appreciation and your capital is not touched. If you want regular income, you should opt for Dividend option.

If you invest in MIP mutual funds through growth option, you would not get any regular payouts, however, your capital would get appreciated till you redeem or sell your MF units. If you do not want regular income, you should opt for Growth option.

How Monthly Income Plan (MIP) Mutual Funds are taxed?

MIP Mutual funds are taxed based on the growth or dividend option chosen by you.

If you have opted for Dividend Option, your mutual fund house need to pay Dividend Distribution Tax (DDT) to Govt before they pay dividend to you. Means, these are tax free in the hands of investors.

If you have opted for Growth Option, when you redeem or sell your mutual fund units, the capital gains are taxed like any other debt fund schemes. If these are sold within 3 years, short term capital gains applicable and you need to club this income with your income and pay income tax based on your income tax slab. If these are sold / redeemed after 3 years, long term capital gains are applicable and the returns are taxed at 10% without indexation and 20% with indexation.

Also Read: HDFC Click 2 Protect 3D Pkus comes with unique features – Should you opt for this plan?

Can we opt for Systematic Withdrawal Plan (SWP) in MIP Mutual funds?

One of the main drawbacks of MIP in mutual funds is, they do not provide guaranteed regular income. In case the returns are lower, these schemes do not declare dividends. Hence, one would get doubt whether there are any alternatives in such case. Systematic Withdrawal Plan (SWP) could answer this question. You can opt for Growth Option in MIP Mutual funds and do Systematic Withdrawal Plan (SWP).

Let me explain with an example. You can invest ₹ 10 Lakhs in MIP Mutual funds with growth option. Assume that you are getting 10% returns per annum and 0.83% per month i.e. ₹ 8,300 per month. Now if you opt for dividend option, you may not get ₹ 8,300 every month as returns could be volatile. In such case, opt for SWP.

Dividend Option Vs Systematic Withdrawal Plan (SWP) – Which is better in MIP Mutual funds?

Here is what dividend option offers.

1) Only capital appreciation is paid out to you. In case there is no capital appreciation, no dividend is paid.

2) Tax on Dividends are paid by MF AMC directly of 12.5%. The amount received in the hands of the investor is tax free.

3) Whether to pay out dividend along with frequency is decided by mutual fund house depending on the returns.

Here is what the SWP option offer.

1) Periodic payout is fixed by the investor. If you want ₹ 5,000 or ₹ 10,000 per month, you decide.

2) If you have capital appreciation, such payout would come from your returns, otherwise, it would be withdrawn from the capital.

3) An investor needs to pay short term capital gain or long term capital gain depending on the start date of the payout. If you opt for payout after 3 years, long term capital gains can be paid.

Top 10 Best Monthly Income Plan (MIP) Mutual Funds to invest in 2017

We have classified Top 10 MIP Plans into Aggressive Funds and Conservative Funds. We picked-up 5 funds from Aggressive MIP Funds and 5 funds from Conservative MIP funds.

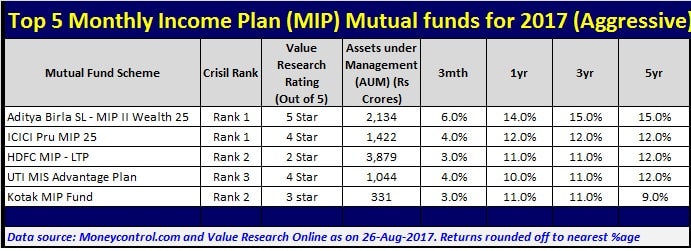

Top 5 Aggressive MIP Mutual funds to invest in 2017

Aggressive MIP mutual funds invest 15% to 30% in equity and balance in debt funds. These are good for investors who want to take a relatively higher risk and expect higher returns. These are high risk high return MIP Mutual Funds to invest in 2017. These Top 5 Aggressive MIP Mutual Funds gave annualized returns upto 15% in the last 5 years.

Top 5 Conservative MIP Mutual funds to invest in 2017

Conservative MIP mutual funds invest up to 20% in equity and balance in debt funds. These are good for investors who want to take a relatively lower risk in debt funds. These Top 5 Conservative MIP Mutual Funds gave annualized returns upto 11% in last 5 years.

Also Read: Top 10 Aggressive Growth Mutual Funds for 2017

Limiting factors of MIP in Mutual funds

Banks offer guaranteed income. However, MIP doe doesn't offer fixed returns. However, this drawback can be removed by opting for the SWP in MIP mutual funds.

MIP returns are volatile and may or may not pay dividend sometime at all.

MIP mutual funds carry some factor of risk as it invests up to 30% in equity.

Conclusion: Monthly Income Plan (MIP) Mutual funds provide regular payouts and they are tax efficient. If you are worried about not getting regular payouts you can opt for the SWP in MIP Mutual funds. This way you can invest lumpsum in your mutual funds and get returns upto 15% per annum. If you observe, some of the funds gave as high as 15% returns in mutual funds which is double the interest rates offered by Bank FD’s in India.

Happy investing in MIP Mutual Fund!!!

If you enjoyed this article, share it with your friends and colleagues through Facebook and Twitter.

Suresh

Top 10 Best Monthly Income Plan (MIP) Mutual Funds to invest in 2017

- 5 Best Small Cap Mutual Funds to Invest in 2026 (Based on Rolling Returns) - July 24, 2026

- How to Select the Best Demat Account? - July 23, 2026

- ULIP vs NPS: Best for Retirement Planning - July 22, 2026

I got good clarity on MIPs. But I wud like to know how MIPs with Dividend option are comparable to Balancecd Fund with Dividend option. And the same for SWP on Growth option in Balanced & MIP Funds.

Hi Shrikant, Good to hear about you. MIP mutual funds aim is to pay regular dividend. However balanced funds on other hand would invest 65% in equity and 35% in debt and look for growth. Both are somewhat similar, however, opt for balanced funds more growth perspective though you are opting for dividend option

i am retired ployee i want to invest 30lacs rs [thirty lacs ] only in various m/f i want atleast 11 to 12 percent monthly pl guide in proper way that there will be very minimum risk & good returned pl early as possible thanks

thanks removed my confusion and given excellent clarity.I am a retiree looking for alternative

to Bank FD with better return.

Sir last 2017 year u r recommend top 5 MIP and top 5 aggressive mutual fund..It's very good idea to investment..

Sir pls recommed for 2018 to invest MIP and aggressive plan

waiting for post

Dear sir

Can you please provide more information about reputed mutual funds with SWP IN MIP where 15% return is available

Thanks and regards

Venkat

Can you please recommned few best combination plans for lumpsum investment for a periodic interest payout. I'm retiree as well and willing to inest 20 lakhs.

Thx in advance

Rajender

Hi,

I am looking for monthly income upon investment (Good to invest 5 laks). Please suggest me which is best. I don’t want to take any risk.

I am a senior citizen who had been investing in FD’s so far. Now, several of them are maturing and I am looking to generate regular income by investing in suitable mf’s.

I notice that some balanced funds are offering monthly or quarterly dividend plans. For example, HDFC Balanced Fund is offering quarterly dividend. HDFC Prudence Fund is offering monthly dividend. These funds are investing 65%+ in equity and so their dividends are tax free and there is no DDT. Of course, the risk is higher in these funds because of the greater equity participation.

On the other hand, the MIP’s of MF’s are treated as debt funds and are subject to the dividend distribution tax. This reduces the return in the hands of the investor. Of course, they are probably less volatile because of lower equity content.

I would like to invest 10 lakhs + for regular income (monthly or quarterly) generation. Should I invest in balanced funds or MIP’s or a combination of both ?

Hi Utpal, Balanced funds are good and can reduce risk as they invest 35% in debt. Means, risk is not elimited. Debt funds invest in debt including corporate debt so some risk is still there (>0% risk). My advice is invest in combination if you would like to take benefit from equity too.

Hi Suresh,

I have a medium/Long team investment intention with Moderately High risk appetite.Currently i am investing 11000 INR monthly in below 3 Mutual Funds :

1. Aditya Birla SL Equity Fund(G) — Large Cap – 3500 INR

2. Mirae Asset Emerging Bluechip-Reg(G) – Small/Medium Cap — 3500 INR

3. Motilal Oswal MOSt Focused Multicap 35 Fund-Reg(G) Diversified — 4000 INR

Could you please suggest if this portfolio looks good to you ?

Secondly , if i want to add in aditional 4000 monthly to this , to make total investment 15000 per month , should i distribute it among the existing MFs ( in what Ratio ?) OR start with new MF ( can you sugest or two options please ? )

Many Thanks.

Ritesh

I would like to invest in mutual fund 1000 per month..suggest me in which mutual fund and in which schme ? Thanks !!

Investing lumpsum into an equity based balanced fund and keeping withdraw date after one year makes it totally tax free

True or false…….

True Raghavendra

List of top 10 MIPs is missing.

Mahavir, like i indicated i segregated 5 into aggressive and 5 into conservative. Both put together are top 10 funds.

Can i withdraw this amount in emergency?