Also Read: LIC Launched Dhan Sanchay Plan 865 – How good is this plan?

What are capital guarantee plans?

Capital guarantee plans are where the capital is guaranteed on maturity of the plan. There are many ULIPs which have high allocation charges, premium allocation charges, management fees etc.. where the capital itself is not guaranteed on maturity. Life insurance companies can float capital guarantee plans where the principal / capital is guaranteed and beyond that, it is not guaranteed.

Max Life’s new plan guarantees 100% capital on maturity.

Key Features in Max Life Smart Capital Guarantee Solution

This is a combination of its Max Life Smart Wealth Plan and Max Life Flexi Wealth Advantage Plan.

This plan provides a capital guarantee through maturity benefit with its Max Life Smart Wealth Plan + market linked returns through part premium paid towards Max Life Flexi Wealth Advantage Plan.

This policy provides flexible premium payment options.

This plan is a comprehensive life insurance plan with death benefit and maturity benefits.

It is a unique life insurance plan that provides benefits by way of lump sum, regular income and whole life benefit depending on the option chosen.

This plan provides an income tax benefit u/s 80c for the premiums paid up to ₹ 1.5 Lacs in a financial year.

Any individual who has a minimum of 18 years can consider this life insurance plan.

The maturity amount is tax free u/s 10 (10D) of the income tax act.

What are various options available?

This plan comes with 5 different combinations.

1) Milestone Solution (10 years)

One needs to pay premium for 5 years after 10 years, policy holders would receive 100% of capital + market linked returns.

2) Milestone Solution (12 years)

Here, one needs to pay premium for 5 years after 12 years, policy holders would receive 100% of capital + market linked returns.

3) Milestone Solution (15 years)

One needs to pay premium for 5 years after 15 years, policy holders would receive 100% of capital + market linked returns.

4) Whole Life Solution

Premium payment term is 8 years and policy term is whole life i.e. 100 years of age. One can get a 100 % capital guarantee by way of income for 8 years. One can make partial withdrawals till 100 years of age.

5) Regular Income Solution

Premium payment term is 6 years, one can get regular income for 30 years after the premium payment term.

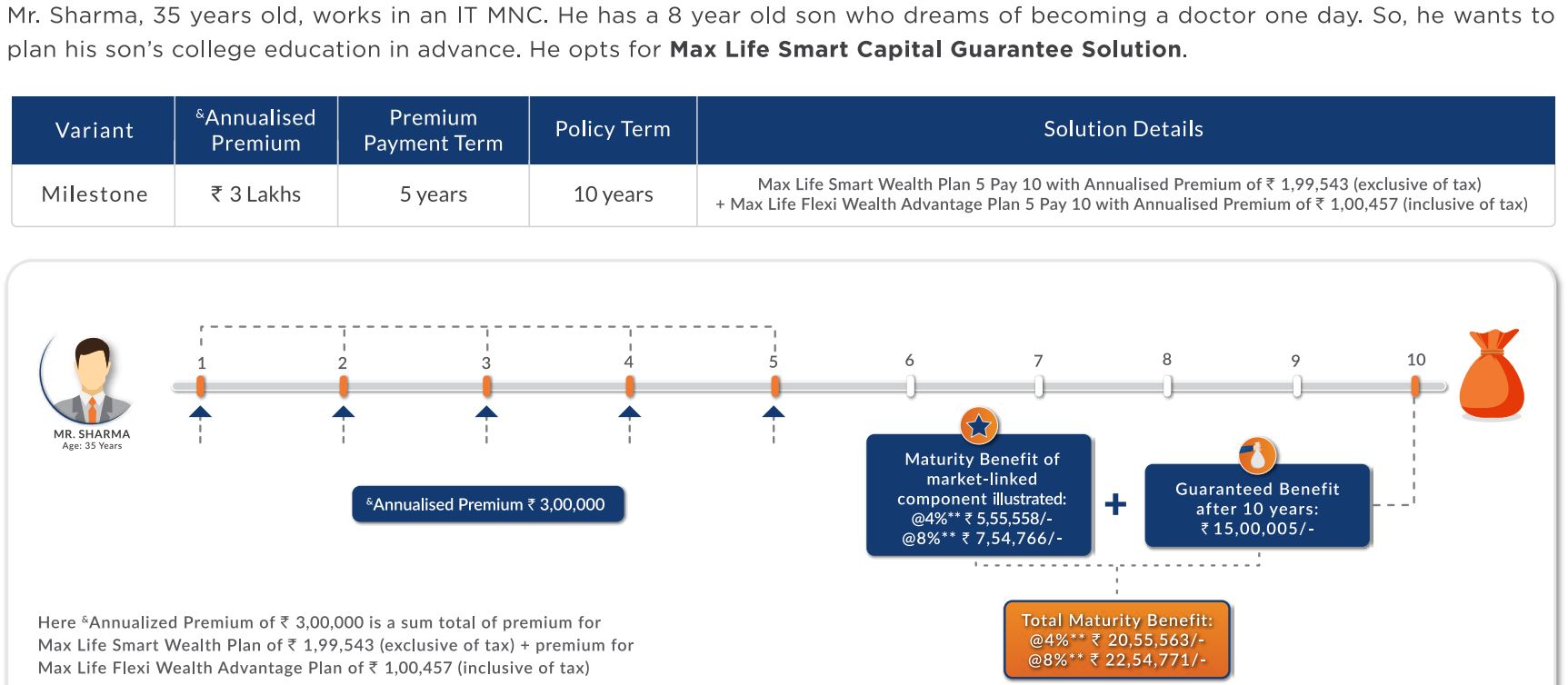

How does Smart Capital Guarantee Solution from Max Life work?

Here is an illustration on how it works (click the picture to enlarge).

Positive Factors in Max Life Smart Capital Guarantee Solution

This is a comprehensive life insurance savings scheme. While it provides life insurance benefits, it also helps to grow savings.

This scheme provides 100% capital guarantee. Investors need not worry about safety of their investments.

This is good scheme who want to invest in a disciplined manner and looking for safe and guaranteed returns.

Negative points in Max Life Smart Capital Guarantee Solution

While there is a 100 % guarantee for capital, there is no guarantee for any returns.

Generally, returns from ULIP plans are not guaranteed. The returns can be negative, however in long run these can generate 4% to 8% returns after all premium allocation charges, management fees etc., Since this is a combination of life insurance and market linked returns, one can assume similar returns.

Also Read: Best Term Insurance Plans in 2022

Max Life Smart Capital Guarantee Solution – Should you opt?

This is a combination of 2 of the existing plans of Max Life. This combination provides 100% capital guarantee returns + market linked returns. While capital is guaranteed, there is no guarantee for returns. Such plans can provide low returns. If you are a low risk investor, want to invest in a disciplined way and looking for safety of capital along with life insurance, you can opt for such plans. Otherwise, one can ignore such plans.

Have you liked our tips and analysis? Then share it on your Facebook, Twitter, Telegram and other social media, which might be useful to your friends too.

How does this fund comparable with ICICI Pru Signature ? It’s also a ULIP policy with some level of capital gurantee…As I am thinking of buying that, your view will be greatly appreciated..Thanks..

While on the face of it, any or this Max Life Smart Capital Guarantee Plan look fine but if after paying premium for five years and waiting for another/further period of , say , 5 years, if I am “entitled” to get only the guaranteed amount, i.e. my invested amount, then, what is the point in it. Would it not make better sense to put the same money in a bank FD or even buy a GoI/RBI bonds giving more than 7% yield as of now for similar or even longer maturity.

I do not know how at the back end, this whole system works. May be that the insurance company would invest 100% amount in GoI/RBI bonds and only the interest received would be invested in the market giving some “extra” return over the maturity period.

Your point is right. LIC Jeevan Shri gives guaranteed return for 5 years and then participation in profits which has mostly matched with guaranteed return of 5% on sum assured or more.

Most banks give 5.5% interest only and out of that TDS of atleast 10% will go.

Is anybody is giving 7%?

Thank you sir. Are the returns taxable? If yes would they come under capital gains tax or would it be taxed according to tax slab

Akash, Any amount received from insurance company is tax free.

Sir, annuities are taxable, right? For example Jeevan Akshay of LIC gives annuity for one time premium. If you pay 12 lakhs, you will get annuity of 1.27 lakhs per year. But it is taxable sir.

Maturity amount from insurance plans are tax free. However, if you buy annuity plan and you get pension income every month/quarter/yearly, then such pension / annuity income is taxable based on income tax slab applicable to the individual