Debt investments are often sold as stable, predictable, and low-risk. But what happens when something that is supposed to protect your capital ends up destroying it? Many investors park their hard-earned money in fixed deposits, corporate deposits, bonds, and debt mutual funds assuming “nothing can go wrong.” Unfortunately, Indian markets have already shown us that even so-called safe debt products can face defaults, downgrades, and liquidity crises. In this article, let us understand what really happens when a debt investment fails — and more importantly, what lessons retail investors must learn.

When “Safe” Turns Into a Scam: Real Examples from India

Before we discuss credit downgrades and liquidity risks, it is important to understand something more dangerous — outright fraud disguised as fixed income products. Over the years, several large-scale scams in India have exploited investors’ trust in so-called safe instruments like bonds, debentures and fixed deposits.

Sahara India Pariwar (2010)

Sahara raised over ₹24,000 crore from millions of small investors through Optionally Fully Convertible Debentures (OFCDs). These instruments were presented as legitimate investment opportunities. However, regulatory authorities later found that the fundraising lacked proper approvals and resembled a massive Ponzi-style structure. Investors believed they were investing in secured debentures — but regulatory gaps exposed the truth.

Saradha Group Scam (2013)

Often referred to as a chit fund scam, the Saradha Group also mobilised funds through redeemable bonds and debentures. Nearly 17 lakh investors were reportedly affected, with collections estimated at around ₹2,500 crore. High return promises were sustained using money from new investors — a classic Ponzi mechanism.

IL&FS Crisis (2018)

The IL&FS default was not a small scam — it was a systemic shock. The group defaulted on debt obligations exceeding $12 billion. What made this event alarming was that several instruments carried high credit ratings until shortly before the crisis erupted. The episode triggered panic in debt mutual funds, led to sharp NAV corrections, and exposed how rating comfort can sometimes create false confidence.

CRB Capital Markets Scam (1996)

The CRB Group collected public deposits and issued debentures across multiple group entities. Instead of deploying funds into productive assets, money was diverted to shell companies. Retail investors suffered heavy losses when the structure collapsed.

DHFL (Dewan Housing Finance Limited) Crisis (2019)

The collapse of entity[“company”,”Dewan Housing Finance Corporation Limited”,”india housing finance company”] (DHFL) was one of the biggest shocks to India’s NBFC space. The company defaulted on repayment obligations in 2019, and subsequent investigations alleged fund diversion and financial irregularities. DHFL eventually went through insolvency proceedings under the IBC framework. Several debt mutual funds, bank depositors, and bond investors faced capital erosion and long recovery timelines.

Shreya Infrastructure Finance Default (2019)

entity[“company”,”Shreya Infrastructure Finance Limited”,”kolkata nbfc”], an NBFC focused on infrastructure financing, defaulted on its debt obligations in 2019. While not structured like a Ponzi scheme, the default highlighted credit concentration risks and the vulnerability of smaller NBFCs dependent on short-term borrowings. Investors in certain debt schemes and NCDs faced steep markdowns following rating downgrades.

These examples show that fixed income risk is not always about business slowdown — sometimes it is about misgovernance, aggressive lending practices, liquidity mismatches, or in some cases, alleged financial misconduct.

Common Modern Fixed Income Fraud Tactics Investors Must Watch

While large scams make headlines, smaller fixed income frauds continue even today in more sophisticated formats.

1. Ponzi Schemes Disguised as High-Interest FDs

Fraudsters promise “guaranteed” returns of 12% to even 48% per annum — far above market rates. Initially, payouts are made using fresh investor inflows, creating trust. Once inflows slow, the scheme collapses.

2. Unregistered NBFC Deposit Schemes

Some entities collect deposits without proper RBI registration. They operate aggressively for a short period, accumulate funds, and then disappear — leaving investors with no legal recourse.

3. Fake Online Investment Apps

Scammers now use WhatsApp groups, Telegram channels, and social media ads to promote fake bond investment apps (for example, apps claiming affiliation with known financial brands). Investors are shown artificial profits inside the app to encourage larger deposits before accounts are blocked.

4. Impersonation of Established Financial Institutions

Fraudsters create websites and brochures that closely resemble reputed banks or NBFCs. They call investors claiming access to “exclusive corporate bond placements” and request transfers to private accounts.

The common thread in all these cases is simple: they exploit the investor’s desire for predictable income and capital safety.

Understanding these scams helps us differentiate between market-linked credit risk and deliberate financial fraud — both of which can severely damage wealth.

Why Debt Investments Are Considered Safe

Debt instruments are designed to generate predictable income. Unlike equity, they promise:

- Fixed interest payments

- Defined maturity date

- Higher seniority in repayment compared to shareholders

Because of this structure, investors assume capital protection is guaranteed. However, “fixed return” does not mean “risk-free return.” The risk simply shifts from price volatility to credit risk and liquidity risk.

The Moment of Shock: What Happens During a Default?

When a company fails to pay interest or principal on time, it is classified as a default. The impact is immediate and painful:

- Credit rating agencies downgrade the instrument sharply

- Market value of the bond falls dramatically

- Debt mutual fund NAV drops overnight.

- Investors panic and try to redeem. As an example check Franklin India Debt Funds issue earlier.

- Liquidity dries up

In some cases, recovery can take years — and sometimes investors never recover full capital.

How Credit Rating Downgrades Destroy Value Overnight

Many investors depend blindly on credit ratings. But downgrades often happen only when problems are already visible.

Chart showing Credit Rating vs Bond Price Impact

This chart shows how a downgrade from AAA to BB can cause 10–30% capital erosion instantly.

This visual will clearly demonstrate that debt instruments are extremely sensitive to rating changes.

Liquidity Crisis: When Investors Rush to Exit

Debt funds work smoothly when inflows are steady. But during fear periods:

- Large investors redeem first

- Fund managers are forced to sell better-quality assets

- Remaining investors are left holding weaker papers

This creates a dangerous cycle.

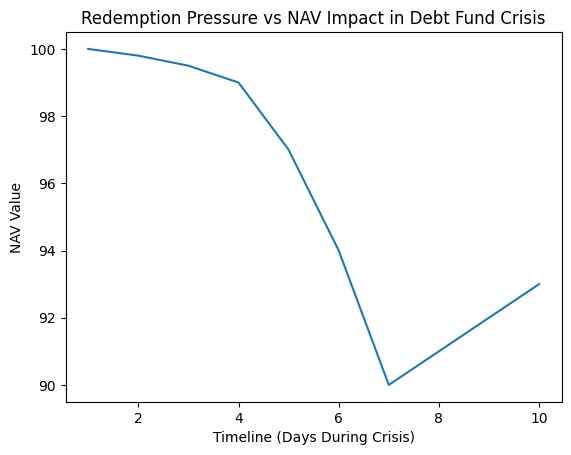

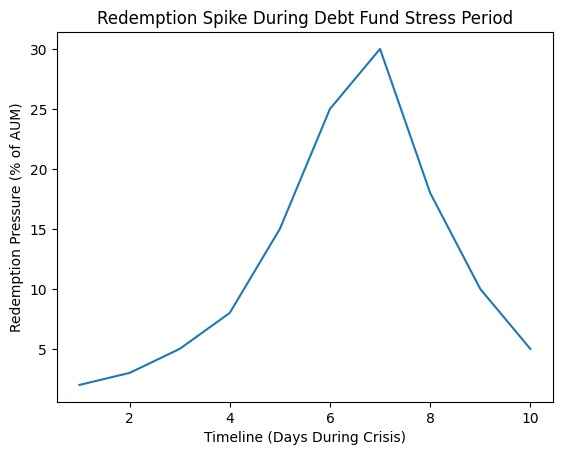

Chart Showing Redemption Pressure vs NAV Impact

- Timeline chart showing redemption spike and corresponding NAV drop

- Highlight how panic selling worsens losses

Such a visual helps readers understand that liquidity risk is real even in debt funds.

Past Debt Defaults That Shocked Indian Investors

India has witnessed multiple high-profile debt stress events in the last decade. Some involved NBFCs, infrastructure companies, and housing finance firms.

These events taught us:

- Even large institutions can fail

- High interest rates often signal higher risk

- Diversification inside a fund does not eliminate systemic risk

The biggest shock for investors was realizing that “debt mutual funds can also lose money.”

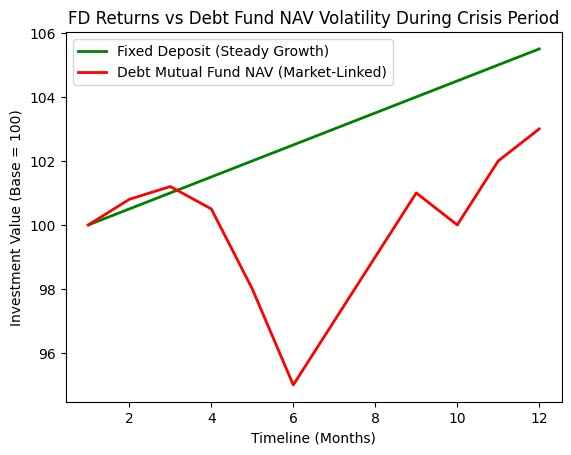

Impact on Debt Mutual Fund NAVs

Unlike bank FDs, debt mutual funds are market-linked. If the underlying bond price falls, NAV reflects it immediately.

Chart showing FD Returns vs Debt Fund NAV Volatility

- Compare steady FD growth line

- Overlay volatile NAV movement during crisis period

This comparison visually reinforces the difference between guaranteed and market-linked products.

Recovery Process: Can Investors Get Their Money Back?

Recovery depends on:

- Company asset quality

- Legal proceedings under insolvency frameworks

- Seniority of debt

- Collateral backing

In some cases, investors recover 40–70% after several years. In others, recovery may be negligible.

Investors must understand that debt recovery is a legal and time-consuming process — not an automatic refund.

Warning Signs Investors Often Ignore

Here are red flags many investors miss:

- Unusually high yield compared to peers

- Concentrated exposure to one group

- Frequent rating outlook revisions

- Aggressive asset growth by the issuer

- Overexposure to stressed sectors

If a product offers 2–3% extra return without clear explanation, that extra return is compensation for hidden risk.

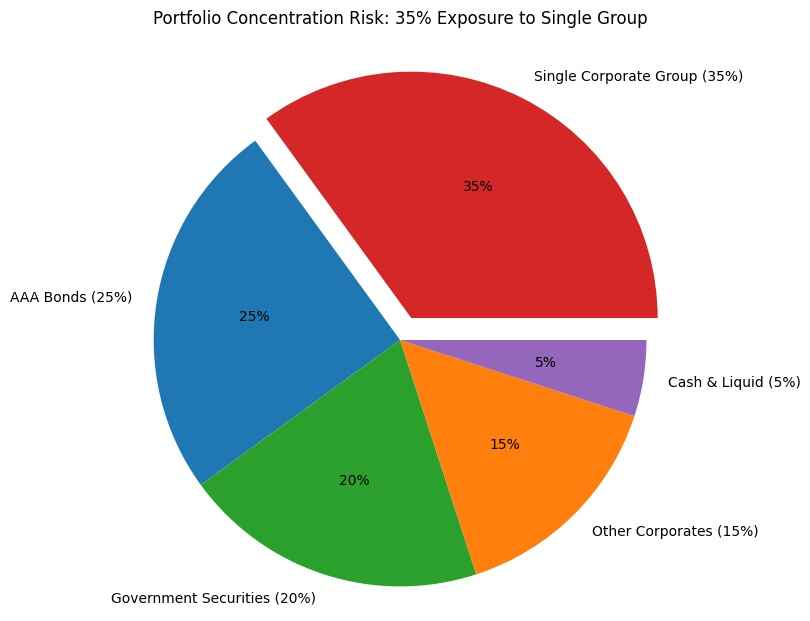

Concentration Risk: The Hidden Danger

Some debt funds load heavily into specific corporate groups or sectors to enhance yield.

Chart showing Portfolio Allocation Risk Pie

Visual storytelling helps readers grasp concentration risk instantly.

Regulatory Reforms and Structural Changes

Over time, regulators have introduced:

- Categorization of debt funds

- Exposure limits

- Side-pocketing norms

- Enhanced disclosure requirements

While these measures improve transparency, they do not eliminate credit risk. Investors must still evaluate risk personally.

Practical Lessons for Conservative Investors

If you are a conservative investor, here are practical safeguards:

- Do not chase yield

- Prefer high-quality, short-duration funds

- Avoid concentrated credit risk funds unless you understand them

- Limit allocation to lower-rated corporate deposits

- Maintain diversification across banks, funds, and instruments

Safety in debt investing comes from discipline, not blind trust.

Checklist Before Investing in Any “Safe” Debt Product

Before investing, ask:

- What is the credit rating?

- What is the portfolio concentration?

- What is the average maturity?

- Who are the top 5 issuers?

- Is the extra yield justified?

If you cannot answer these clearly, reconsider the investment.

Final Thoughts: Safety Is Relative, Not Absolute

Debt investing is not about eliminating risk. It is about understanding and managing it.

The biggest lesson from past defaults is simple — there is no such thing as completely safe investing. Every extra return comes with an invisible risk attached.

Instead of asking, “Is this safe?” a better question is:

“What could go wrong here — and am I prepared for it?”

That shift in thinking can protect your portfolio far better than any credit rating ever will.

Thank you Suresh for a very informative read. After having fallen victim to Ponzi Scam (Creditbulls Investments), for me it is Once Bitten, Twice Shy. Hence I have bookmarked your website and visit it often to get more insights from an expert like you. Thanks again.

For senior citizens the First priority should be SCS Scheme upto Rs 30 lacs with safe 8.2% returns, guaranteed by GO I.

Thank you for your comments.

Yes, the Senior Citizens’ Savings Scheme (SCSS) is indeed a strong option for retirees seeking stable income. With returns backed by the Government of India, it offers a high level of safety compared to market-linked debt products.

However, investors should also consider factors like interest rate reset risk, investment limits (₹30 lakhs), and overall portfolio diversification.

For senior citizens, capital safety and predictable income should certainly remain the top priority.

Perfect analysis highlighting risks in a supposedly safe debt investment/instrument. In this heightened risk taking environment (partly by stock market continuous boom and partly by general economic growth optimism), the risk of a debt instrument getting default is always there. Flurry of debt/NCD issues recently is a pointer in this direction.

One must be cautious because protecting capital is crucial than earning from the capital.

Thank you for your insightful observations Kamalji.

You are absolutely right — during periods of strong market optimism, investors tend to underestimate credit risk. The recent increase in NCD and debt issuances does indicate rising borrowing appetite, which makes careful evaluation even more important.

As you rightly said, in debt investing, capital protection should always take priority over chasing higher yields.

Appreciate your thoughtful contribution to the discussion.

Thank you very much for the detailed explanation on debt crash. You have been sending several recommendations with detailed explanation. May I request you to add few columns viz. 1. Promotor’s names and their back ground. 2. What is there percentage of share in the share capital. 3. Share holding pattern 4. Marketability of their products etc. 5. Debt Service Coverage Ratio.

Please advise about companies dealing with Semiconductor industries and car batteries etc. Thank you. Regards

Thank you very much for your valuable suggestions and kind words.

Your points on promoter background, shareholding pattern and DSCR are well noted. While these are very important for equity analysis, in debt investing the key focus is usually on cash flows, leverage, interest coverage, liquidity position and credit rating — since repayment capacity matters more than ownership structure.

I will try to include additional financial metrics like DSCR wherever reliable data is available.

Regarding semiconductor and car battery companies, these are capital-intensive and fast-growing sectors. I will plan a separate detailed article covering fundamentally strong companies and their risk profile.

Thank you once again for your feedback.