Irrespective of the fact that whether it is your first job or you are an experienced professional, a certain portion of your salary may be deducted in the form of income tax. Moreover, the tax is levied not only on your basic salary, but other allowances that prominently reflect on your salary slip. What are the various ways salaried individuals can save income Tax in India? What are the various precautions salaried individuals should take to avoid any income tax demand in future?

Also Read: Best Tax Saving Options in India for 2017

What is Cost To Company (CTC)?

The total of your basic salary, conveyance, and other benefits is known as the Cost to Company (CTC). It is the cost which your employer incurs to bring you on the payroll, and the tax is computed on it.

As said by Benjamin Franklin, “In this world, nothing is certain but death & taxes”, therefore, you can’t avoid taxes at any cost. However, there are some components in your CTC, which can curtail your tax liability and boost your take home salary. Before we discuss them, let’s first know under which slab your income falls:

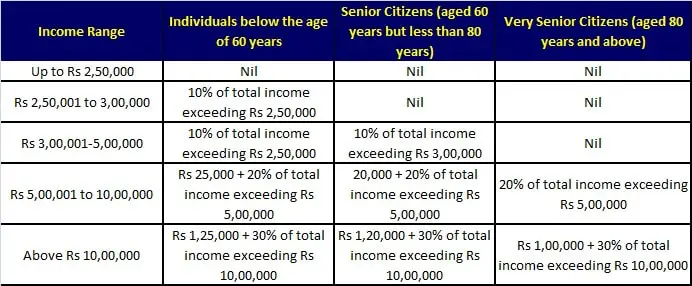

What are income Tax Slabs for the Financial Year 2016-17?

Here is the income tax Slabs for this financial year.

Tax slab remains the same for both men and women.

In case of individuals earning below ₹ 5 lakhs, the tax rebate has been raised to ₹ 5,000 from ₹ 2,000 under Section 87A.

3% education cess is levied on income.

In case of the individuals earning above ₹ 1 crore, the surcharge has been raised to 15%.

8 Ways Salaried Individuals Can Save Income Tax in India

1) Make use of the Section 80C (Maximum Tax Exemption Limit: ₹ 1.5 lakhs)

Under the Section 80C, the maximum tax deduction limit is ₹ 1.5 lakhs. You can invest in any of the following options to save tax:

- Public Provident Fund (PPF)

- EPF (Employees Provident Fund)

- Post office tax saving deposits

- National Savings Certificate (NSC)

- Equity Linked Savings Scheme

- Kid’s tuition fees

- Senior Citizen Savings Scheme (SCSS)

- Home loan principal repayment

- National Pension Scheme (NPS)

- Life insurance premium

- Sukanya Samriddhi Scheme

You can invest in National Pension Scheme for additional ₹ 50,000 u/s 80CCD.

2) Think beyond the Section 80C

If you have exhausted your 80C limit, here are some more options for you:

Section 80D: You can secure your health and save taxes also. The health insurance premium is eligible to get tax deductions up to ₹ 25,000. For a senior citizen, the limit is ₹ 30,000 and for a very senior citizen, (who is above 80 years), the deduction is ₹ 30,000 towards medical expenses. Even the preventive health checkup is tax-exemptedu p to ₹ 5,000. Note, it is not over and above the individual limits mentioned below. Further, if you opt for top-up and super top-up policies, you can also get the similar tax benefits.

Section 80DD and Section 80DDB: You can claim up to ₹ 75,000 on the medical treatment of dependents who have 40% disability under the Section 80DD. In the case of severe disability, the tax deduction limit is ₹ 1.25 lakhs. However, to claim deduction under this section, it is mandatory to submit a medical certificate issued by a specialist doctor working in any hospital— government and private.

Similarly, medical expenses incurred on the treatment of critical ailments qualify for tax benefits up to ₹ 40,000 under Section 80DDB. In case the age of the insured is between 60 years and 80 years, the deduction limit is ₹ 60,000 and for super senior citizens (above 80 years), the limit is ₹ 80,000. Some of the diseases which are covered under this section are cancer, neurological diseases, chronic renal failure, and hematological disorders.

Section 80G: Contributions made towards certain charitable institutions and relief funds are tax exempted if made via cheque, draft or in cash. However, no exemption is given for donations that are made in cash exceeding ₹ 10,000.

Section 80GG: It is given to those people who neither own a residential house nor get the HRA. The tax deduction limit has been raised to ₹ 60,000/annum.

Section 80E: If you have taken a loan for higher studies, you are eligible to get the tax benefit. It is maximum offered for a tenure of 8 years or till the entire interest is paid, whichever is earlier.

Section 80TTA: The deduction up to ₹ 10,000 is offered on the interest received on the saving deposit with a bank or post-office.

Section 24: Under this section, you can avail tax deductions up to ₹ 2 lakhs on the interest of the loan taken for the purpose of construction/acquisition of self-occupied house property.

Section 80EE: If you have taken a home loan for the first time, you can get an additional deduction of ₹ 50,000 on the home loan interest, provided the following conditions are met:

House loan should be sanctioned in the financial year 2016-17

Home loan amount should not be more than ₹ 35 lakhs

House value should not exceed ₹ 50 lakhs

Home buyer should not have any property registered in his/her name.

You may like: Ways your parents can save income tax for you

3) Housing: To rent or to live in a company provided flat?

It is easy to live in a flat given by your employer rather than going for house hunting. However, do bear in mind that rental payment can help you in getting tax benefits against the house rent allowance (HRA). On the other hand, the company provided flat would be taxable.

Let’s look into these two options in detail:

HRA

It is considered as one the most common parts of CTC. People staying in a rented accommodation can get tax exemption against the HRA received, and the remaining amount would be taxed. In this case, the least of the following three would be tax-free:

(a) Actual HRA received from the company

(b) Actual rent you pay in excess of 10% of the basic salary

(c) 50% of the basic salary if the house is in a metro city: Delhi, Mumbai, Kolkata or Chennai, and 40% of basic salary in case of other cities

In case you don’t have the HRA component in your salary, the maximum tax deduction is ₹ 5,000/month or ₹ 60,000/yearly.

Note, if your annual rent is more than ₹ 1 lakhs, it is mandatory to submit the copy of your landlord’s PAN card along with the rental receipts to your accounts department.

Flat given by an employer

The perquisite value is decided on the basis of the fact that whether the flat is owned by the company, taken on rent for you or is a hotel accommodation given to you.

In case it is a hotel accommodation, the value will not be more than 24% of your salary and 15% of the salary in other cases. In case the company’s accommodation is furnished, another 10% of the cost of furnishing or actual hire charges is added to the total value of perks.

Note, if you move to a new city, the hotel accommodation given by your employer for the first 15 days is not taxable.

4) Leave Travel Concession (LTC)

Your annual vacation in India can give you tax benefits also. The tax exemption is limited to the shortest airfare available for your destination. However, no exemption is given for expenses like conveyance, hotel, etc.

Note that you have to submit travel bills to claim the deduction. Also, your travel expenses for a foreign holiday are not eligible for the tax break. If you decide to cover various destinations in India as well as a foreign destination during one trip, you may not get tax benefits even for your domestic trips.

5) Leave encashment

You have the option to encash your entitled leaves either on resignation or retirement. Though tax rules for leave encashment are detailed; the maximum exemption limit is ₹ 3 lakhs. Note that any leave encashment during the work tenure is taxable.

6) Other allowances and tax benefits

Transport Allowance: Any allowance amount paid by your employer to meet the daily conveyance requirement is tax exempted up to 1,600/month.

Note that it is not required to submit any expense proof for claiming the exemption. However, if expenses are incurred on the official travel, your employer can reimburse your expenses on the basis of the bills submitted by you.

₹ 2,400/month plus ₹ 900/month applies if the cubic capacity of the engine is more than 1.6 litres. However, if the capacity is less than or equal to 1.6 litres, the value of perquisite will be ₹ 1,800/month plus ₹ 900/month.

Children’s education allowance: With the help of this component, you can get tax benefits of ₹ 100/month and ₹ 300/month for education and hostel expenses, respectively. However, this benefit is restricted to two kids only.

7) Other reimbursements

There are certain reimbursements which are exempted from tax, like medical expenses up to ₹ 15,000/year and the reimbursement of telephone expenses. However, in the case of telephone expenses, there is no limit prescribed for the maximum amount that can be availed, your employer can levy an internal cap for this reimbursement.

8) Retirement benefits

Gratuity: If you change your job after five continuous years or retire after a service of more than five years, you will get a gratuity amount. While, there are detailed rules on the exemption, the maximum amount exempted is ₹ 10 lakhs.

Employee Stock Ownership Plans (ESOPs): Mainly, these are used by companies, especially startups, to retain talented employees. Under this scheme, an employee can buy shares of the company at a discounted rate. Mainly, it has three important stages:

Grant: – As it is the first stage, an employee is given the option to buy certain shares.

Vesting:- An employee receives an unconditional right of shares. However, the employee doesn’t possess an actual share at this stage.

Exercise: By paying a pre-decided amount, an employee can get the right to acquire shares. Post allotment, an employee can either hold or sell these shares.

Mainly, ESOPs are taxed at the following two stages:

Stage 1: On the share allotment stage, the difference between the Fair Market Value (FMV) of shares and the exercise price is considered as the taxable income.

Stage 2: At the time of sale of shares, the difference between the sale price and the fair market value on the date of exercise is considered as capital gains and taxed accordingly.

Smart tips to restructure salary slip and cut tax

It is not easy to restructure your salary, but if your company allows you to do so, restructure a few components of your salary to curtail tax liability:

Instead of lunch allowance, opt for food coupons as they are exempted from tax up to ₹ 50/meal

Make transport allowance, medical allowance, uniform expenses (if any) and education allowance a part of your salary. You would need to submit original bills of these expenses to curtail tax liability

Instead of using the personal car, opt for the company’s vehicle to cut down the high prerequisite tax.

Also Read: How to file income tax returns in 15 minutes in India?

An illustrative example to understand the tax outgo

Let’s understand the salary structure of three salaried people – Surinder, Rahul and Ajay. Also, let’s find out the ways they save tax:

*We have assumed that all medical bills are submitted.

Conclusion: Submit all your investment proofs before hand to avoid any tax deduction. Carefully check the Form 16 received from the employer. Start your tax planning well before 31st March and don’t wait until the last minute. Consider all tax saving options.

Happy Tax Saving!!!

If you enjoyed this article, share it with your friends and colleagues through Face book and Twitter.

Suresh

Ways Salaried Individuals Can Save Income Tax in India

- 5 Best Small Cap Mutual Funds to Invest in 2026 (Based on Rolling Returns) - July 24, 2026

- How to Select the Best Demat Account? - July 23, 2026

- ULIP vs NPS: Best for Retirement Planning - July 22, 2026

Well illustrated ..n well explained…thanx GURU

Dear Suresh,

A Good informative article, thank you !!

Superb explanation..! First time I understood about how to save Income tax. Thanks alot for sharing all the possibilitis.

Your explanation is so simple that even a layman can understand. Appreciate your knowledge and explanation skills.

Thank you, keep up the good work

Thank you Pavendhan

looking to understand tax rebate

looking to understand tax rebate

This article was really good

Hi suresh,

i owned house and paying loan too and getting benefit of principle and interest as per tax benefit.can i avail HRA benefit??

Dipak Maheshwari

Dear Suresh

The housing loan will come extra exemption(1.5+2 lakh) or include of (1.5+50=2lakh) base exemption.

Please explain this,

So basically, you should submit all your investment proofs before hand to avoid any deductions. Carefully checking the form 16 given by the employer and that's all. You're done.

Thank you for your advice.

I am archshaa house wife.last year only i've start invest in share market.my husband is NRI. I invest my husband money. how about my tax? pls advice…