Couple of days back, Canara HSBC OBC Life Insurance has a launched a new ULIP plan called Secure Bhavishya Plan. Canara HSBC OBC Life Insurance Secure Bhavishya Plan says it protects and meets individual future financial life. This plan helps custom build a retirement fund which can be used for steady post retirement income. How good is Bhavishya Plan from Canara HSBC OBC Life Insurance? Should you opt for Canara HSBC Oriental Bank of Commerce Secure Bhavishya Plan for your retirement planning? In this article, I would review this retirement aimed plan.

Couple of days back, Canara HSBC OBC Life Insurance has a launched a new ULIP plan called Secure Bhavishya Plan. Canara HSBC OBC Life Insurance Secure Bhavishya Plan says it protects and meets individual future financial life. This plan helps custom build a retirement fund which can be used for steady post retirement income. How good is Bhavishya Plan from Canara HSBC OBC Life Insurance? Should you opt for Canara HSBC Oriental Bank of Commerce Secure Bhavishya Plan for your retirement planning? In this article, I would review this retirement aimed plan.

Features of Canara HSBC OBC Life Insurance Bhavishya Plan

- It offers Guaranteed Maturity Benefit of 101% of premiums paid, including top up premiums (if any), provided all insurance premiums are paid before maturity.

- It offers unlimited top ups of premiums that can be paid depending upon your retirement need.

- Various options to choose maturity age and premium payment term.

- Flexible premium payment options including monthly and yearly.

- Loyalty Additions (LA) would be added to your fund starting from 10th year, after every 5 years.

Also Read: Should you opt for Max Life Online Term Plan?

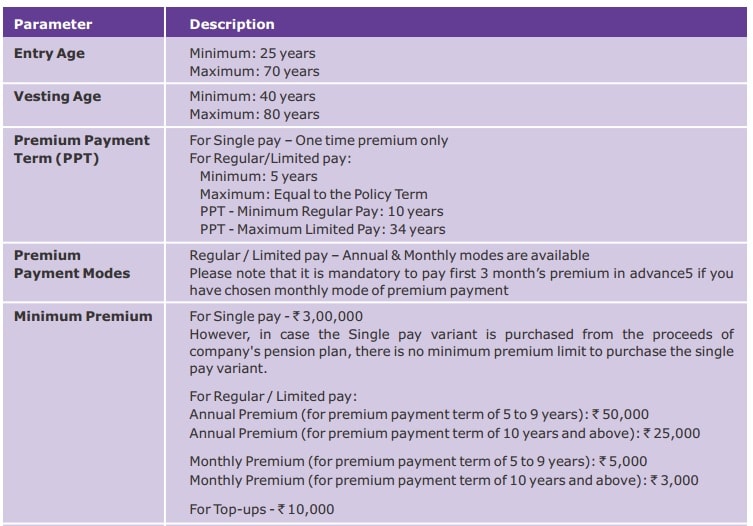

What is the eligibility details for this plan?

What are various benefits available in Canara HSBC OBC Life Insurance Bhavishya Plan?

a) Death Benefit

Higher of Fund Value or 105% of the total premiums paid.

How nominee can utilize the death benefit?

The nominee has an option to utilize the death benefit either to Utilize the entire proceeds of the policy / part thereof for purchasing an immediate annuity or withdraw the entire amount of the policy.

b) Maturity Benefit / Vesting Benefit

Higher of Fund Value or guaranteed maturity benefit, where the guaranteed maturity benefit is 101% of total premiums paid including top up premiums)

What options available on maturity?

1. Get the amount to the extent allowed under prevailing laws and balance amount to purchase an immediate annuity only from them. This would be guaranteed for life, at the then prevailing annuity/pension rates.

2. Utilize the entire proceeds to purchase the single premium Pension plan from the Company.

3. Extend the accumulation period or defer the maturity date for the same policy, provided you are less than 55 years of age as of that date.

Also Read: HDFC Click 2 Retire ULIP comes with low allocation charges – Is it really good plan?

How does this plan work exactly?

- Choose any retirement age between 40 to 80 years with a minimum policy term of 10 years and maximum policy term of 35 years.

- Choose any premium payment term from 5 years up to the vesting / retirement age. You can also choose a single premium option in this plan.

- Choose the premium amount you want to invest in the chosen premium payment term

This plan well explained with an example

Mr. Rajendran is a 40 years aged working professional wants to plan for his retirement and build-up a retirement corpus, which enables him to get a guaranteed income post his retirement at age 60. He estimates that after meeting all his current and future expenses, he would be able to invest an amount of INR 10,000 per month for the period of 20 years. He also values the flexibility to invest more (through top-ups) whenever he has some extra money for his retirement corpus. Furthermore, he wants to invest some part of his premiums into equities for higher growth, but at the same time he requires capital protection to safeguard his investments from the market volatility.

- Retirement / Vesting Age: 60

- The total amount invested = Rs 24 Lakhs

- Guaranteed Vesting Benefit = Rs 24.24 Lakhs (101% of premiums paid)

- Total vesting benefit @ 4% returns = Rs 30.52 Lakhs. Annuity payable based on current annuity rates is Rs 2.14 Lakhs per annum for life time.

- Total vesting benefit @ 8% returns = Rs 46.7 Lakhs. Annuity payable based on current annuity rates is Rs 3.28 Lakhs per annum for life time.

What are various investment funds available?

What are the various charges under this plan?

The allocation charges will be deducted upfront and will be levied through reduced premium allocation to the fund.

Premium allocation charges: It charges upto 5.4% to 8.4% from 1st year to 10th year. See below table for complete details.

Policy administration charges: It would be 0.05% of the annualized premium chargeable on monthly basis during the first five policy years. Thereafter it will increase by 20% every five years staring from the 6th policy year. However, this charge will not exceed `500 per month in any case.

Mortality charges: Charges of Rs 1.16 to Rs 12.687 per every 1000 fund value would be charged as mortality charges. See below table for complete details.

Fund Management Charges (FMC) : 0.5% to 1.35% as FMC charges would be levied. See below table for complete details.

Also Read: All you wanted to know about Unit Linked Insurance Plans

Should you invest in Canara HSBC OBC Life Insurance Bhavishya Plan?

Now you have complete clarity about the savings plan. Its basically a ULIP plan which invests in 3 funds based on your investment objective / age. For all your premiums, they would deduct various allocation charges like premium allocation charges, policy administration charges, mortality charges and fund management charges. These comes to over 8%. Means from your investment done every year upto 8% would be deducted (or charged) and balance is invested in ULIP fund. Even assume that your fund has performed well and gave 12-15% returns, after deducting allocation charges, you can expect net returns of 5% to 7% with life insurance coverage (105% of premiums paid). This is what you want? Just think before you take any step to invest in such so called retirement schemes.

If you enjoyed this article, share it with your friends and colleagues through Face book and Twitter.

Suresh

Canara HSBC OBC Life Insurance Bhavishya Plan

- How a 5K SIP Can Fetch You Rs 1.8 Lakhs per Month Fixed Income in Mutual Funds in 30 Years? - April 16, 2024

- Bandhan Innovation Fund NFO – Issue Details and Review - April 14, 2024

- I’m 40, Have 30 Lakhs, Where Should I Invest in Mutual Funds? - April 13, 2024

– Benefits and Review")

Hello,

I had very bad experience dealing with Canara HSBC ULIP Policy. I had this policy linked to my NRI account but when I return last year I decided to surrender this policy as I had already completed 5 yrs of locking period. After couple of weeks, I got a reply saying that 30% tax will be deducted from the fund value and the balance will be transferred to my account. It took 4 mths to get my full due money after very long exchange of telephonic discussion / e-mail communication. I had a real hard time to get my well deserve dues. So guys, please be careful while dealing with them. Ask them in detail about the procedure of surrendering and getting your dues and also if possible get it in writing.

Tks a lot for detailing the plan.

Nobody will be happy with this combination as returns seems to be very low. Instead of this one may opt for TERM PLAN for family cover and MF SIP route for RETIREMENT GOAL .

Regards.